One of the most widespread misconceptions about economics is that it’s all stocks and bonds and funds. While those certainly play a large role, economics goes beyond finance, as a tool to explain why society and its people do the things we do. Interwoven with law, politics, education, and the environment, among others, economics bridges all facets of life, proving that outcomes are rarely the result of merely a few factors. As the intersection between psychology, the study of mind and behavior, and economics, the study of incentives and resource allocation, behavioral economics seeks to explain why we sometimes make choices questionable to others, and maybe even ourselves. In other words, behavioral economics is the study of economic behavior but from a psychological perspective. It is considered to be in the field of economics known as microeconomics.

If you have ever wondered why people act irrationally, then you have already indirectly engaged with behavioral economics. Unlike traditional economics, behavioral economics tosses aside the assumption that humans are rational. Rather, it assumes that humans are irrational but that we can identify our motives and thus justify our decisions. It stands to reason that, as irrational humans, we make errors, act on impulse, and are immensely impressionable. Behavioral economics aims to study why that is so.

We are not thinking machines. We are feeling machines that think.

Antonio Damasio, USC Neuroscientist

Prospect Theory

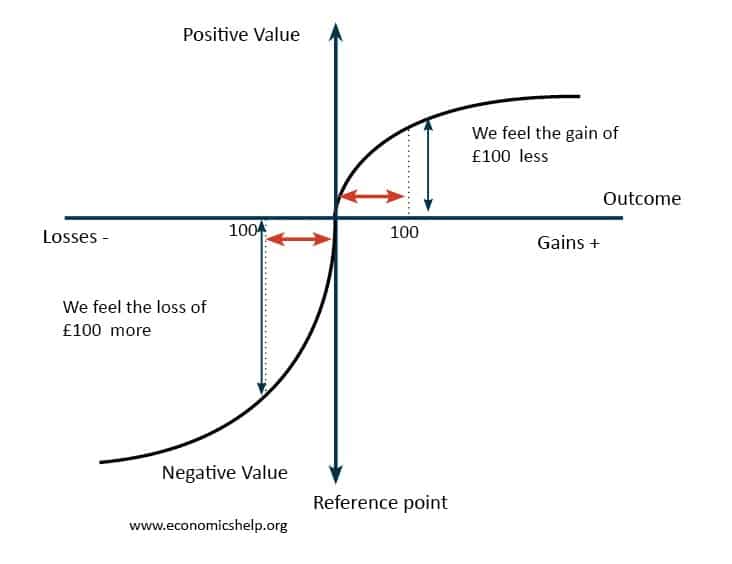

The history of behavioral economics began with two professors, Daniel Kahneman of Princeton and Amos Tversky of Stanford. They focused on people’s attitude toward risk, or the degree of uncertainty, under different circumstances. Together, they developed prospect theory, or the idea that people treat numerically equivalent losses and gains differently. In other words, when weighing two equal possibilities of gain and loss, people react differently. Further known as loss-aversion theory, investors as well as consumers have long instinctively prioritized avoiding losses to achieving gains.

Kahneman and Tversky found that when presenting two options: getting $1000 with 100% certainty or getting $2500 with a 50% certainty. Most people opted for certainty over a higher reward. Unsurprisingly, people were content with settling for less, knowing that they secured a financial gain. However, Kahneman and Tversky flipped the situation of the two choices by turning the gains into losses. Presented with a certain loss of $1000 versus a 50% chance of either no loss or a $2500 loss, the majority of subjects preferred the second option, running the risk that they might lose substantially more, but hoping that they might walk away having lost nothing.

Kahneman and Amos Tversky hypothesize that the distinct risk-taking decision between the first and second scenario derives from the greater emotional impact perceived from losses versus gains. Losses seem to have twice the negative value as a positive gain of equal magnitude. In other words, losses hurt twice as much as gains when they are of the same magnitude.

Bounded Rationality

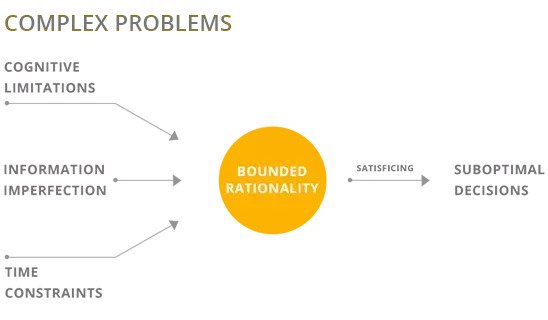

To rationalize a decision, we expect a certain level of information. Yet, as with the case of purchases, we typically don’t know everything about the item, person, or idea. Surface level observations may lack a proper explanation of how they came to be that way, such as low prices. When presented with an incomplete picture, we tend to fill in the gaps with our own flawed assumptions. Economist Herbert Simon called this bounded rationality. Bounded rationality is the principle that there exist limits to information, time, and thinking capacity. Therefore, there are natural limits to how far our rational mind can effectively make choices.

Framing Effect

Besides a lack of information, or perhaps excessive emphasis on a particular factor, people often make decisions based on not only what the information is, but also how it is presented. While we’d like to believe we, if not necessarily rationally, can point to the exact reasons why we made a decision, in doing so, we may fail to recognize the true, underlying motives. Known as the framing effect, this form of bias explains the specific choices advertisers make and how that ultimately influences consumer behavior.

Ever seen an item, like clothing, food, or a book, priced just below a whole number? It may seem silly to some, but charm pricing, one of many psychological pricing tactics, is an age-old strategy businesses employ to make their products seem more attractive. For example, the rational mind may see $7.99 as $8. But, the irrational, average customer will treat it closer to $7.

On the flip side, some companies are notorious for elevating their prices past justifiable levels, essentially overvaluing their own product. Instead of investigating, however, many people buy into it, as demonstrated in a Stanford study examining levels of enjoyment in relation to varying wine prices. Contrary to conventional logic, as prices increased, so did enjoyment, even as the wine quality itself stayed constant. This is due to the notion that wine that is more expensive is perceived to be of much better quality. Therefore, consumers were more willing to buy a more expensive wine even when nothing indicated it was of better quality. This is behavioral economics in action.

Nudge Theory

If you want people to do something, make it easy.

Richard Thaler, Father of Behavioral Economics and professor at the University of Chicago

University of Chicago Professor Richard Thaler’s guiding principle encapsulates the concepts he pioneered in a book he co-authored, Nudge: Improving Decisions About Health, Wealth and Happiness. Armed with a variety of tools at their disposal, companies, schools, and governments can change consumer opinions, student behavior, or civilian actions without changing the existing options or removing the undesirable ones. Nudge theory maintains that people make decisions based on a combination of our own biases, the information presented to us, and how it’s presented to us.

Thaler argues that the process called choice architecture encompasses both the noticeable options as well as the not-so-easily noticeable context with which the options are laid out for us. In consequence, choice architects can design not only the presentation of choices but also the results themselves. By taking advantage of subconscious thoughts and biases, choice architects can direct behavior to their personally favorable outcome. Thaler encourages us to learn to identify the hidden nudges behind our daily decisions, whether it be at the voting booth or in the shopping mall. Take a step further, and you’ll see that nudges can be useful tools to conquer bad behavior and cement the good.

Rearranging or redefining the choices you offer yourself, such as setting up an automatic enrollment plan for retirement, stocking your pantry with healthier snacks, or scheduling exercise sessions ahead of time, are all effective ways of guiding your own behavior for the better. In Thaler’s words, harnessing the power of nudges opens the door to libertarian paternalism. Libertarian paternalism is his philosophy that guiding influences can peaceably coexist with freedom of choice.

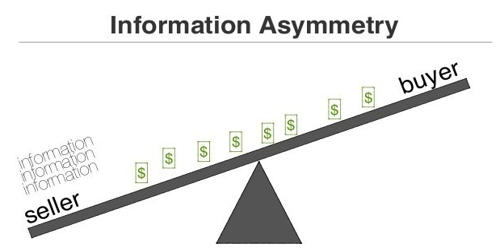

Information Asymmetry

As established, traditional economics makes the assumption that people are rational. This implies that when people engage in some kind of economic interaction, whether money is present or not, everyone involved in the interaction has the same information. Having the same information as all other participants is known as information symmetry. For example, the stock market, in theory, has investors that all invest based on publicly disclosed information. Therefore, everyone has access to it and there should be information symmetry.

But in many cases, including the stock market today, there have been instances of information asymmetry, or the idea that in an economic interaction of buying and selling, one side has more information than the other. Economist George Akerlof, in his groundbreaking paper “The Market for Lemons,” introduced this idea of information asymmetry. Akerlof studied the used-car market and was able to determine that at a certain point, only “lemons,” or low-quality used cars, would be sold in that market. He called high-quality used cars “peaches.”

Essentially, the used-car market was made up of buyers and sellers, but the buyers don’t know whether the used-car they were buying is a peach or a lemon while the sellers obviously do. The buyers, knowing that the car they could be buying could either be a peach or a lemon, play it safe by not offering to pay as much for a peach but not as low as a lemon. The buyers come in wanting to buy a used car at a price in between the peach price and the lemon price for that car, often at the average price.

Now, a used car seller would see that offer from a buyer and choose to sell that buyer a lemon. Why? The buyer is offering to pay a fixed price that is an average price of a peach and a lemon. That price is inherently a higher price than the price of a lemon. The seller, knowing which of his cars are truly lemons, will offer a lemon. That way, the seller can receive from the buyer a price that is higher than the lemon’s actual price. The seller would refuse to sell a peach to the buyer because the buyer is offering to pay a price that is lower than the true price of a peach.

In other words, because the buyer is unaware of which cars are peaches and which cars are lemons, he or she is neither willing to pay a full, higher peach price in fear of being ripped off nor willing to pay just the lower price for a lemon in order to be competitive for a higher-quality used car. But the seller, because of the knowledge of which used cars are truly lemons, can find an opportunity to sell lemons for a price higher than that lemon’s true price. The buyers aren’t willing to pay for a full peach, so sellers, in response, don’t sell those peaches.

This creates a cycle in which buyers continue paying lower and lower prices. Sellers keep taking the peaches out of the market in response to lower and lower prices. Akerlof called this adverse selection. Eventually, the only cars that sellers will try to sell will be lemons. Hence, the title “The Market for Lemons” for Akerlof’s paper arises and with it a Nobel Prize in 2001.

Akerlof introduced the idea that information asymmetry in markets can have damaging effects. In the used-car market, it can drive out the good quality cars and leave only lemons through the adverse selection that results from information asymmetry. This can lead to market failures.

This ties into behavioral economics because people engaging together often have uneven knowledge of information. When people are incentivized to behave dishonestly, they can take advantage of that information asymmetry. This creates certain conditions that favor them but perhaps not others.

Behavioral Game Theory

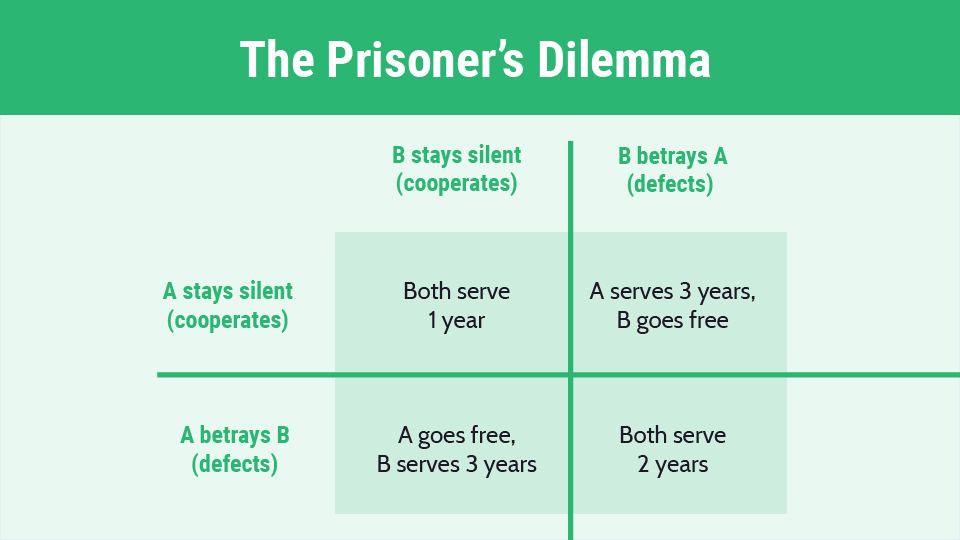

Game theory is the study of strategic decision-making amongst multiple people or entities. Traditional game theory uses rational choice theory. Rational choice theory is basically the idea that humans are rational decision-makers and make decisions that benefit them the most. A simple example of game theory is the prisoner’s dilemma, pictured below.

Prisoner’s dilemma poses a hypothetical situation in which you have two inmates, A and B, who must cooperate or betray in regards to a criminal charge. Now if A stays silent, B can either stay silent by confessing and cooperating or betray A by denying and defecting, and vice versa. Let’s look at each of the scenarios:

- A and B both stay silent, they both serve 1 year

- A and B both defect, they both serve 2 years

- B stays silent and A betrays B, then A goes free and B serves 3 years

- A stays silent and B betrays A, then B goes free and A serves 3 years

What would each do if both were rational but had no knowledge or control of the other prisoner’s decision? Well, if A stays silent, B has two choices: cooperate or betray. Rationally, B would betray A because if A is staying silent, then B betraying A leads to B’s freedom. A would suffer 3 years. If B stays silent, A has the same two choices: cooperate or betray. Similarly, A would betray B because if B is staying silent, then A betraying B leads to freedom. Similarly, B would suffer for 3 years. So this would rationally rule out either prisoner choosing to stay silent because of the risk that the other would betray.

Now, if A betrays B, then B’s options are to stay silent and serve 3 years or betray and serve 2 years. Rationally, B chooses to also betray A in order to get the shorter of the two sentences. The same is also true when B chooses to betray A; A would also choose to betray B to get the shorter sentence. This way, both prisoners, by knowing what each option’s outcomes are but not knowing what the other prisoner will choose to do, can rationally arrive at the decision to betray no matter what the other prisoner will do. If one betrays, the other one will as well to get a better outcome, based on the scenario laid out. This is one example of game theory in action.

Behavioral game theory takes into account that all humans are not rational and that they have irrational tendencies. Traditional game theory would claim that every person would act rationally to benefit themselves. But behavioral game theory argues that a person would have a complex set of biases that make them act irrationally. One example is the Dictator Game. In the Dictator Game, one person, the “dictator,” is given a sum of money. The dictator then decides to send a portion of that money to the second player.

Traditional game theory, with rational choice theory at its core, would predict that the dictator would choose to send nothing to the second player and hoard all the given money. Yet, when behavioral economists went out to test this game in the real world, they found that the majority of dictators decided to give a certain sum of money to the second player, a decision that makes no rational sense.

As stated earlier, when given money, it’s irrational to give that money away as people want to maximize their gains. But, the Dictator Game showed that people act irrationally and choose to give some money away to the second player. That is an act of generosity and altruism. While the second person may not have any control over the decision of the dictator, perhaps other factors do, such as society’s view and self-image. These underlying biases that individuals have about those external factors form the basis for behavioral game theory.

Irrational Exuberance

Another way we see irrational behavior take center stage is in the stock market. To maximize profits, investors must accurately evaluate the intrinsic value of an asset, rather than relying on the market value. Intrinsic value is the true value of a company or asset and changes relatively little. The latter depends on the current stock price, possibly fluctuating wildly alongside public sentiment. When investors begin to simply feel optimistic to the point where they pay less attention to the intrinsic and fundamental qualities of the stock market, i.e. how companies are actually performing, and pay more attention to the speculative psychological aspects. This leads to stock prices based on psychology, speculation, and irrationality instead of ones based on fundamentals and rationality.

These markets all have a certain amount of irrational exuberance, a term Nobel Prize-winning economist Robert Shiller coined in his book Irrational Exuberance and Alan Greenspan later popularized. Periods that had heightened irrational exuberance are periods like the dot-com bubble or the financial crisis of 2008. Investors in this period paid attention only to the excitement that the Internet or the housing market caused. These investors failed to look into the fundamentals of what was driving the stock market. Instead, they let bias and unjustified optimism take over. In a nutshell, this is what irrational exuberance is.

Conclusion

Behavioral economics is a relatively new innovation in the field of economics. Behavioral economics combines theories from psychology, neuroscience, and traditional economics. It seeks to explain at a deeper level why humans behave the way they do, especially why they act irrationally. Its recent popularity in recent decades has made behavioral economics a top tool and field that all kinds of people look to for insights. As it continues to evolve, it is likely that behavioral economics will continue providing new ideas as to how people behave with implications for policy, financial markets, and individual people.

Pingback: Behavioral economics: What is it? What are its applications? – PublicFrontLine